Surviving the Debt Cycle with Elastic Assets

Debt is the silent engine of the global economy. It builds growth during the good years and crushes nations when the bill comes due. Every empire, every government, every household knows the cycle: borrow, expand, overextend, collapse, reset.

The pattern is always the same. Debt piles up, confidence falters, and eventually money itself is manipulated to “solve” the problem whether by printing more, devaluing, or just delaying the inevitable. That’s how every debt cycle ends, with fragile money absorbing the shock.

The major problem is that traditional forms of money aren’t built to handle this. Fixed supplies create crushing deflation when credit contracts. Pegged systems break under pressure, forcing bailouts or abandonment. Debt is elastic, but money has been rigid and that mismatch is why collapses hit so hard.

But what if money could bend instead of break? That’s where elastic assets like Ampleforth’s AMPL come in to change the story.

Unlike fiat, AMPL isn’t pegged to a government promise. It’s built to track the long-term purchasing power of the 2019 U.S. dollar, automatically adjusting supply to account for inflation. That means it can absorb shocks instead of breaking under them. In practice, when demand and liquidity surge, supply expands; when demand contracts, supply tightens. Holders still keep the same share of the network even as supply flexes with conditions. That matters in debt cycles because many collapses happen when money stays rigid while debt stretches. Elastic assets move with the stress instead of snapping.

History and Modern Stress Tests

History is littered with examples of what happens when money can’t adapt.

In France, the revolutionary government turned to assignats. paper money printed to cover state deficits. At first, it looked like a solution. But the presses kept running, and trust evaporated. Within a few years, savings were wiped out and the currency collapsed.[1]

In Weimar Germany, money printing fueled such extreme hyperinflation that by late 1923, wages had to be paid multiple times a day and spent immediately, as prices were doubling within hours.[2]

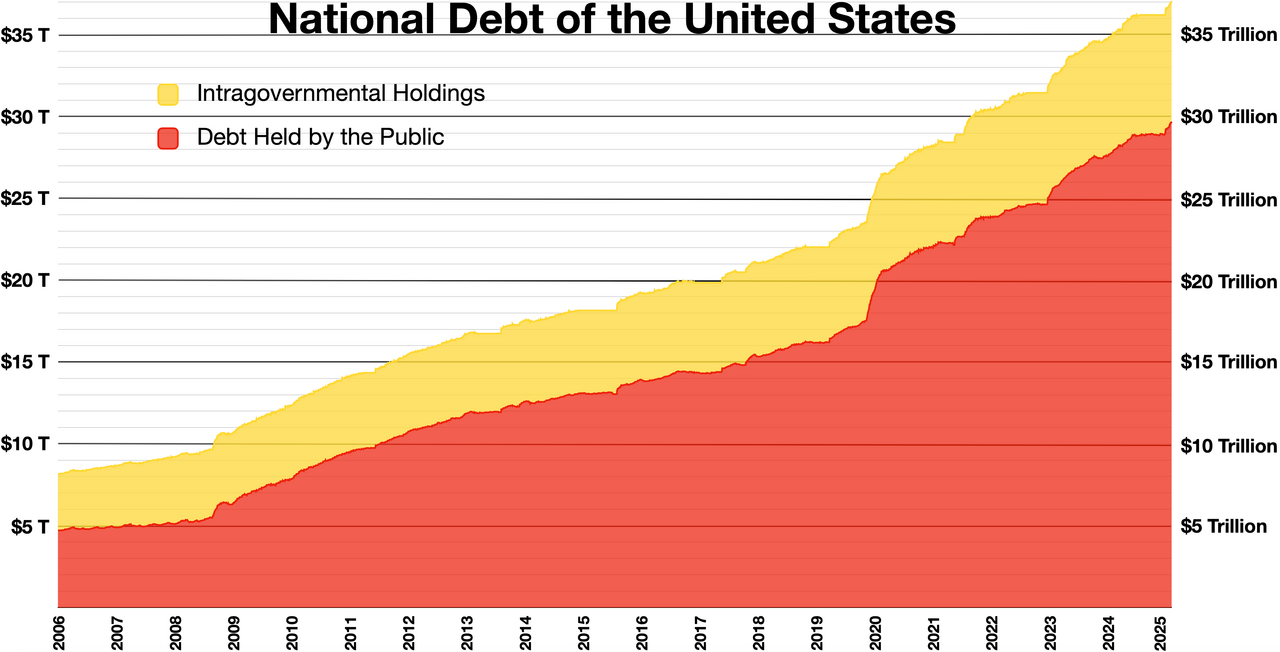

Today, the U.S. leans on the Federal Reserve to juggle over $37 trillion in federal debt.[3][4][5]

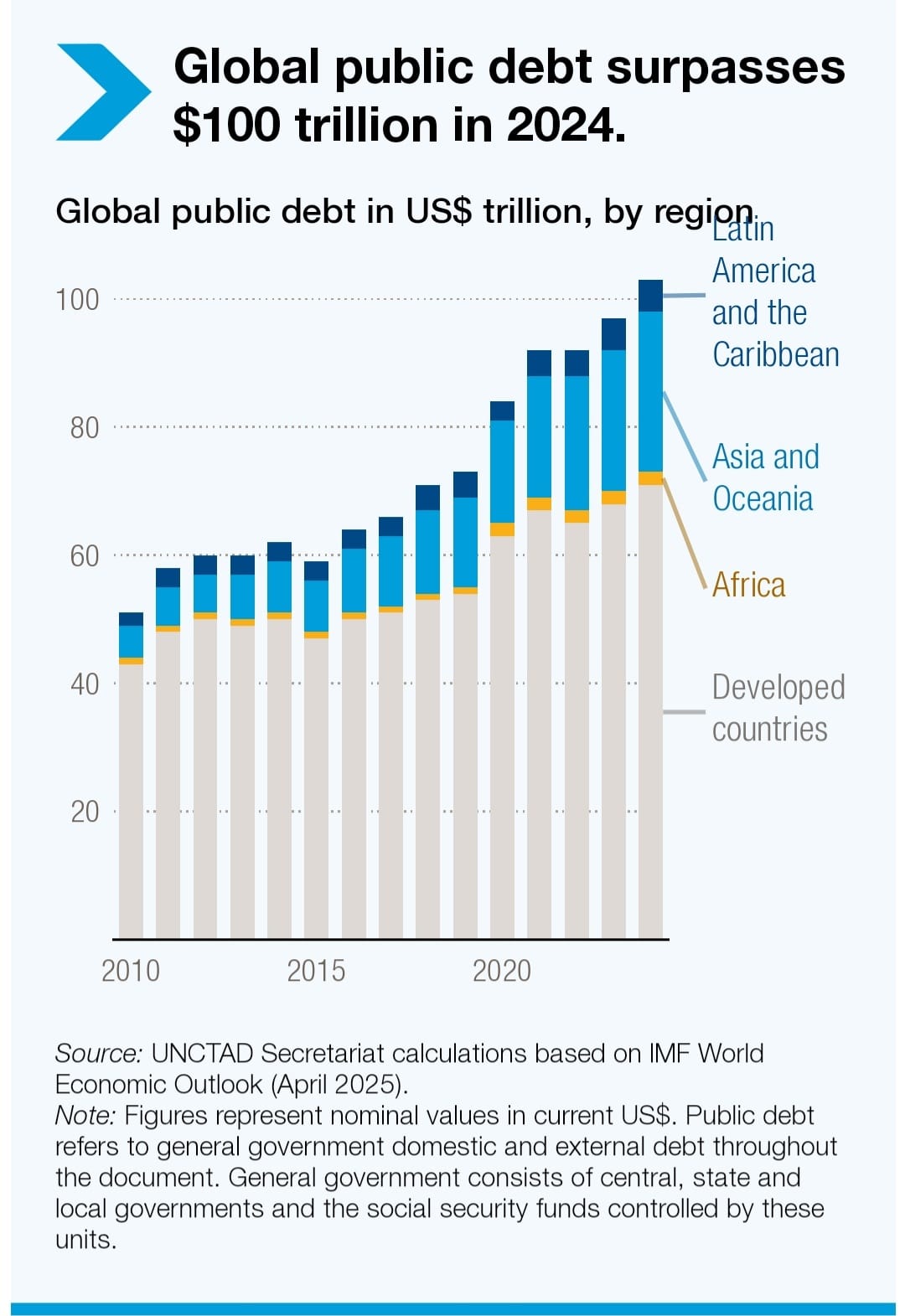

Debt isn’t just a national problem. Globally, public debt recently crossed $100 trillion.[6]

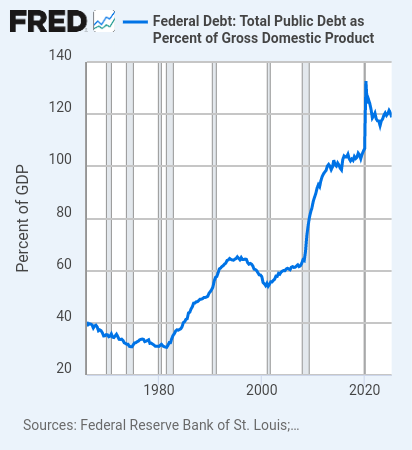

In advanced economies, average government debt is already over 110% of GDP. The U.S. federal debt alone is over 118% of GDP in mid-2025.[7]

When debt-to-GDP gets this high, even small policy missteps can cascade. Currencies unravel. Bonds collapse. People lose faith. That’s where rigidity fails.

Looking Forward: Where Cycles Bend or Break

Case studies show us two paths:

Collapse under rigidity – Countries like Zimbabwe or Venezuela show what happens when governments inflate rigid fiat systems until they snap. Debt overwhelms the currency, and hyperinflation follows.[8]

Adaptation through flexibility – Singapore, for instance, uses a managed float and trade-weighted currency basket, keeping debt moderate and reserves strong to cushion shocks.[9]

Elastic assets like AMPL offer a third way: built-in resilience without depending on central bankers, reserves, or national discipline.

Why Elastic Assets Matter Now

Mismatches vanish: If you borrow in AMPL, your debt expands or contracts with supply. That removes the shock when traditional money hyperinflates or devalues.

Stress absorption: Because supply reacts to demand, sudden liquidity squeezes or panics don’t break the system — they get buffered instead of amplified.

Alignment with inflation: Instead of resisting inflation (and losing purchasing power), elastic money flows with it, preserving long-run stability.

A New Question for the Next Cycle

Debt isn’t going away. Governments will borrow, households will borrow, and cycles will repeat. The real difference lies in what kind of money you hold while it happens.

Elastic assets give us a foundation that bends with stress instead of cracking under it. Where other systems need bailouts, peg maintenance, or national guarantees, Elastic money runs on built-in code and incentives.

When the next debt wave hits and it will, the question isn’t whether debt breaks something. The question is whether your money survives by bending. That’s the promise elastic assets bring to the table.

Sources

[1] The Cobden Centre – Economic Ideas: Inflation, Price Controls and Collectivism During the French Revolution (2016). https://www.cobdencentre.org/2016/11/economic-ideas-inflation-price-controls-and-collectivism-during-the-french-revolution/

[2] EconLib – Hyperinflation (n.d.). https://www.econlib.org/library/Enc/Hyperinflation.html?utm_source=chatgpt.com

[3] U.S. Treasury – America’s Finance Guide: National Debt. https://fiscaldata.treasury.gov/americas-finance-guide/national-debt/

[4] Peterson Foundation – The National Debt Is Now More Than $37 Trillion. What Does That Mean? https://www.pgpf.org/article/the-national-debt-is-now-more-than-37-trillion-what-does-that-mean/

[5] Wikipedia – National Debt of the United States. https://en.m.wikipedia.org/wiki/National_debt_of_the_United_States

[6] UNCTAD – World of Debt: A Growing Burden to Global Prosperity (2023). https://unctad.org/publication/world-of-debt

[7] Federal Reserve Economic Data (FRED) – Federal Debt: Total Public Debt as Percent of Gross Domestic Product. https://fred.stlouisfed.org/series/GFDEGDQ188S

[8] Cato Institute – Zimbabwe: From Hyperinflation to Growth (2009). https://www.cato.org/development-policy-analysis/zimbabwe-hyperinflation-growth

[9] Business Times – Monetary Policy Explainer: How Singapore Uses Its Exchange Rate to Manage the Economy. https://view.ceros.com/businesstimes/monetary-policy-explainer/p/1