From TIPS to Tranching: LVAs Offer Bounded Volatility in a High-Risk World

The global macro environment has reached an inflection point that traditional portfolio theory hasn't fully prepared us for. Policy uncertainty has spiked to 8.3 standard deviations above historical means, the dollar faces its most serious challenges since Bretton Woods, and institutional investors are discovering that correlation breakdowns have rendered traditional hedging strategies ineffective precisely when they're needed most. This convergence of fiscal unsustainability, geopolitical fragmentation, and failing diversification strategies has created an urgent need for entirely new approaches to risk management.

Lets dive into Low Volatility Assets (LVAs), an emerging asset class that reimagines how stability can be achieved in financial markets. LVAs leverage volatility tranching to segment underlying asset volatility into separate low and high volatility components. This reduces the dramatic price swings of underlying assets while preserving meaningful exposure to their long term growth potential. For macro investors grappling with an environment where bonds and equities move in lockstep, LVAs represent an innovation that addresses the core challenge of our era. Mainly, how to achieve genuine diversification when traditional correlations have collapsed.

Traditional hedging strategies face unprecedented limitations

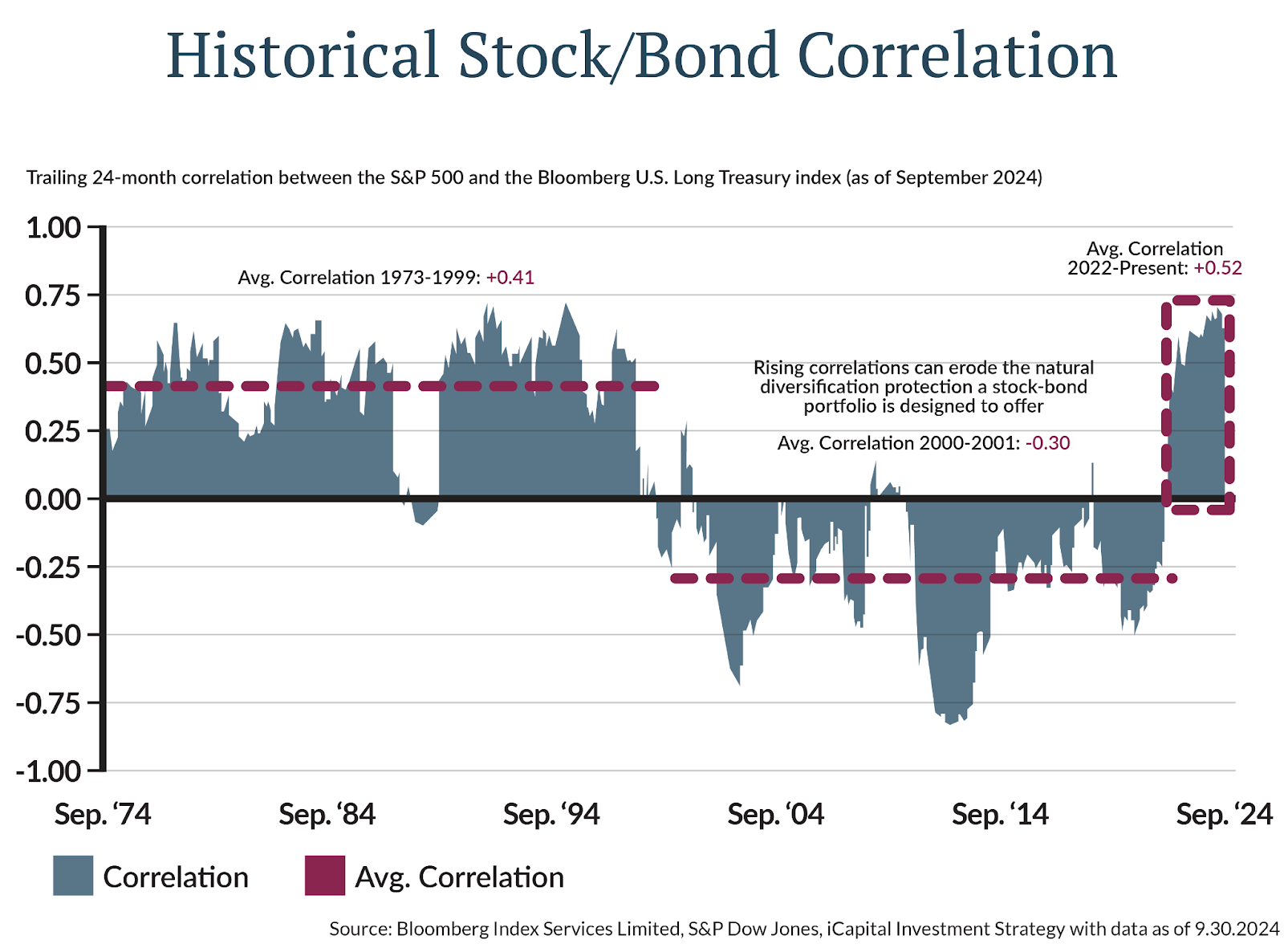

The foundation of modern portfolio theory where diversification provides a "free lunch", has been undermined by a fundamental shift in market dynamics. Stock/bond correlations have reached 0.44, the highest since 1997, while the fraction of market correlations explained by key factors has declined from 95% to 86%. During stress periods, multi asset portfolios face the nightmare scenario where defensive assets like treasuries actually sell off alongside equities, a pattern that violates decades of established relationships.

Treasury Inflation-Protected Securities (TIPS), long considered the gold standard for inflation hedging, have struggled in an environment where real yields remain elevated despite persistent inflation concerns. Meanwhile, traditional safe haven assets have become unreliable. Treasuries now exhibit unusual behavior during market turmoil, rising when they should be falling, while gold's safe-haven properties have become inconsistent across different crisis types.

The challenge extends beyond correlation breakdown to fundamental questions about the dollar's role as the global anchor asset. With US national debt at $36.2 trillion representing 98% of GDP and foreign ownership of US debt declining from 49% to 30% over the past decade, the structural foundation underlying traditional "risk-free" assets faces unprecedented pressure. BRICS nations have accelerated dedollarization efforts, with trade between Russia and China now 95% conducted in non-dollar currencies, while central banks added over 1,000 tons of gold reserves for the third consecutive year.

What makes Low Volatility Assets fundamentally different

Low Volatility Assets represent a major shift from traditional risk management approaches by employing volatility tranching, the systematic segmentation of underlying asset volatility into separate low and high volatility components. This financial engineering technique, familiar to traditional finance professionals from CDOs and structured products, redistributes rather than eliminates market exposure.

The core mechanism works by taking volatile underlying assets and creating senior tranches (low volatility) and junior tranches (high volatility) from the same exposure. Senior tranches receive downside protection while maintaining upside participation. Junior tranches absorb excess volatility from senior positions in exchange for leveraged exposure to positive performance. Crucially, total market exposure is preserved; no value is destroyed, only redistributed according to different risk preferences.

This differs fundamentally from traditional approaches. Derivatives based hedging eliminates risk through offsetting positions, often creating drag on positive performance. Portfolio diversification spreads risk across assets but limits returns to lowest common denominator performance.

LVA implementations achieve this through distinct tranching approaches. Ampleforth's SPOT uses "perpetual tranching" by bundling multiple ‘fixed-term’ vintages of tranches and then systematically rotating maturing tranches out, in exchange for fresh tranches. This allows for a continuous claim on the underlying.

Future LVA implementations like lvBTC (low volatility Bitcoin) and lvGOLD (low volatility Gold) will likely employ similar tranching principles, segmenting Bitcoin and gold volatility into low and high volatility versions while maintaining full exposure to underlying asset performance.

Tranching enables superior capital efficiency

The capital efficiency advantages of volatility tranching over traditional risk management can be compelling for institutional investors. Consider targeting 10% volatility exposure to a 15% volatility asset:

Traditional portfolio approach requires 67% allocation to the target asset with 33% in cash/low-risk assets. This creates cash drag that reduces overall returns.

Tranched structure approach deploys 100% capital in senior tranches that achieve 10% effective volatility through junior tranche subordination. Capital efficiency improves by 49% while maintaining identical risk characteristics!

Unlike principal protected notes that depend on issuer creditworthiness, LVAs achieve capital preservation with reduced counterparty risk. Unlike commodity ETFs that face contango costs from futures rolling, LVAs provide direct synthetic exposure without derivatives complexity.

If we compare with TIPs both mechanisms adjust for external factors, but where TIPS adjust monthly and require government backing, LVAs can employ continuous rebalancing through smart contract execution.

LVAs represent logical evolution in monetary history

Understanding LVAs requires recognizing their place in the millennia long evolution of monetary systems. The classical gold standard (1870s-1914) achieved long term price stability with average annual inflation of only 0.1%. However, it came at the cost of short term volatility and economic rigidity. When the Bretton Woods system collapsed in 1971, it unleashed a persistent search for stability that has driven financial innovation for over five decades.

Each monetary transition has produced new instruments to address specific stability challenges. The move to floating exchange rates in the 1970s spurred the derivatives revolution(i.e Black-Scholes options pricing model). The stagflation crisis led to inflation-protected securities (TIPS). The 2008 financial crisis accelerated digital payment innovation (bitcoin/fintech). LVAs emerge from the current crisis of correlation breakdown and currency system stress, representing the latest iteration in humanity's ongoing attempt to balance stability with flexibility.

Historical precedent suggests that disruptive monetary technologies follow predictable adoption patterns: private sector experimentation, institutional recognition, and eventual mainstream integration. The Chicago Board of Trade revolutionized commodity risk management in 1848. TIPS gained institutional acceptance after inflation concerns in the 1970s-80s. Similarly, LVAs address fundamental needs that have persisted across different monetary regimes - the eternal tension between maintaining purchasing power and adapting to changing economic conditions.

The technical feasibility of LVAs reflects advances unavailable to previous generations. Reliable oracle networks provide tamper resistant price feeds. Battle tested smart contract platforms enable automated execution without counterparty risk. Composable DeFi infrastructure allows seamless integration with existing financial systems. These technological foundations make possible what traditional instruments promised but couldn't fully deliver: stability without sacrificing meaningful participation in underlying asset performance.

Tranching mechanisms offer institutional advantages

For institutional investors, LVAs present compelling technical advantages that address persistent portfolio challenges. Consider hypothetical implementations:

lvBTC would employ tranching to segment Bitcoin's volatility into low and high components. Senior tranches (lvBTC) would provide bounded volatility exposure to Bitcoin's long-term appreciation potential while maintaining the composability benefits of direct token ownership for DeFi strategies. Junior tranches would absorb excess volatility in exchange for leveraged upside exposure. The specific tranching mechanism would matter less than the outcome: constrained downside with preserved upside participation.

lvGOLD could offer inflation hedging superior to traditional gold ETFs by eliminating storage costs, insurance requirements, and authorized participant complexities. The tranching mechanism would automatically segment gold price movements into stable and volatile components, providing pure commodity exposure without operational overhead. Senior tranches would achieve bounded volatility while maintaining proportional participation in gold's performance during inflationary periods.

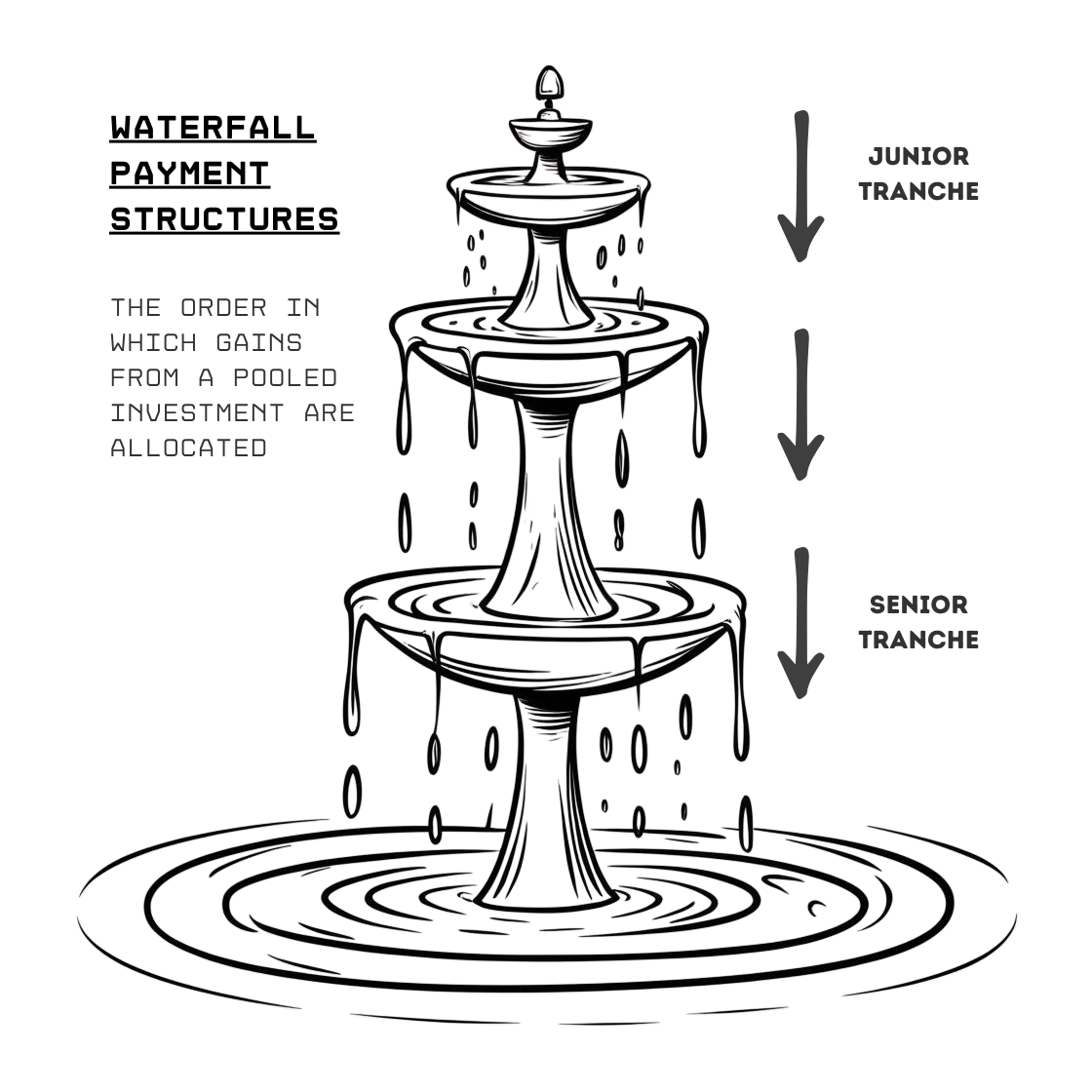

The framework underlying these implementations draws from established structured finance principles. Waterfall payment structures prioritize senior tranches during distributions while maintaining proportional participation in growth. Risk redistribution through structural subordination creates the fundamental value proposition, enabling different risk appetites to access appropriate exposure from the same underlying assets.

Current environment creates unprecedented opportunity

The macro environment of 2025 presents ideal conditions for LVA adoption. Policy uncertainty at historic levels makes traditional economic models less reliable, creating demand for instruments that function independently of government backing or central bank intervention. The breakdown of traditional correlations means institutional investors must fundamentally reassess risk management approaches.

Most critically, the structural challenges facing dollar denominated assets create space for alternative stability mechanisms. With interest payments on federal debt exceeding $1 trillion annually and foreign demand for treasuries weakening, the foundation of "risk-free" assets faces legitimate questions about long-term sustainability. LVAs offer a path to stability that doesn't depend on fiscal sustainability or geopolitical dominance.

The timing also reflects technological maturity.

- Oracle infrastructure has reached institutional reliability standards.

- Smart contract platforms have demonstrated security through billions of dollars in value locked.

- Ampleforth and SPOT have survived downturn events and effectively recovered without breaking.

- Regulatory frameworks are evolving to accommodate programmable money.

These conditions create a window for institutional experimentation with tranching-based volatility management before traditional systems face more serious stress. Vitalik makes a lot of the same points in his article. “Low-risk defi can be for Ethereum what search was for Google”

For macro focused investors, LVAs represent more than a new hedging tool, they offer systematic exposure to the next phase of monetary evolution. Early institutional adoption could provide both portfolio diversification benefits and strategic positioning for a world where traditional monetary anchors prove less reliable.

The emerging asset class thesis

Low Volatility Assets represent a fundamental innovation in how financial markets achieve stability. By employing volatility tranching to segment underlying asset volatility into low and high components, LVAs address core challenges that have become acute in the current macro environment: correlation breakdown, currency system stress, and the search for genuine diversification.

The convergence of technological capability, institutional need, and monetary system pressure creates conditions analogous to previous periods of financial innovation. Just as the collapse of Bretton Woods drove derivatives development and the 2008 crisis accelerated digital finance (bitcoin & fintech), current macro instability is creating space for new approaches to risk management and value storage.

Volatility tranching, whether implemented through Ampleforth's SPOT or future innovations yet to be developed, provides the core mechanism that makes LVAs possible. By redistributing rather than eliminating market exposure, tranching enables stability without sacrificing the growth potential that makes assets attractive to institutional investors.

For traditional finance professionals, LVAs deserve serious consideration not as speculative instruments but as logical solutions to persistent institutional challenges. The tranching mechanisms may be novel in their digital implementation, but they address ancient problems: maintaining purchasing power, managing volatility, and preserving value during monetary transitions. The mathematical principles that created investable instruments from mortgage pools can create volatility-managed assets from crypto portfolios.

The real question isn’t if new ways to create stability will appear as they’re bound to, now that old hedging strategies are breaking down. The real question is whether institutional investors will see LVAs as a smart advancement in financial tools or just another short-lived crypto fad. Given today’s macro trends, it’s likely that LVAs will turn out to be a wise move, especially for those looking to escape the growing risks of highly correlated traditional assets.

As monetary systems face their most significant stress since the 1970s, Low Volatility Assets offer a pathway to stability that doesn't depend on government guarantees, central bank intervention, or geopolitical dominance. For macro investors navigating an unprecedented environment of policy uncertainty and correlation breakdown, LVAs may represent not just a new asset class, but a necessary evolution in how modern portfolios achieve genuine diversification through sophisticated volatility tranching rather than simple hedging or costly derivatives strategies.