Traditional 60/40 models struggle amid inflation and volatility. Low-Volatility Assets create a “Goldilocks zone” for investors - neither too risky nor too stagnant- offering balanced exposure to commodity-money performance.

The retirement-investment landscape stands at an inflection point. Traditional equity-bond allocation models - long treated as axiomatic - are being tested by a trifecta of persistent inflation, heightened market volatility, and rapidly evolving investor needs. At the institutional level, fiduciaries must also contend with tightening regulations and demographic pressures that challenge long-held assumptions about asset-liability matching. Together, these forces have pushed portfolios into what industry veterans dub the “messy middle”: a zone where conventional bonds no longer guarantee real purchasing-power preservation, yet direct exposure to commodity-monies such as gold and Bitcoin introduces levels of variance most mandates cannot tolerate.

Amid this disruption, Ampleforth’s Low-Volatility Assets (LVAs) - most prominently low-volatility Bitcoin (lvBTC) and low-volatility Gold (lvGold) - emerge as a novel asset class engineered to bridge that gap. Powered by the SPOT protocol, Ampleforth’s volatility-tranching partitions an underlying commodity-money into senior, low-volatility claims and junior, high-volatility claims. The resulting senior tokens retain the durability, censorship resistance, and inflation hedging of hard assets while exhibiting price behavior more commonly associated with fiat stability. In effect, LVAs respond to the long-standing market call for instruments that are “much less inflation-prone than fiat monies” yet “much more stable than commodity monies,” without sacrificing uncensorability.

The strategic significance is pronounced in Target Date Funds (TDFs), which today steward more than $4 trillion—growing at roughly 30 percent annualized over the past fifteen years—and already serve as default retirement vehicles for millions of participants. Because TDF glide paths depend critically on assets that can both dampen sequence-of-returns risk and safeguard real value, LVAs present a timely solution for re-architecting those trajectories. Beyond TDFs, the broader institutional arena commands $8.5 trillion in alternative allocations and is poised to reach a projected $2.1 trillion addressable market by 2030. Early adopters that weave lvBTC and lvGold into their strategic asset-allocation frameworks stand to capture superior risk-adjusted returns while materially enhancing retirement security for beneficiaries.

This report outlines how, why, and where LVAs can be integrated across institutional and retail portfolios, with a particular emphasis on their capacity to revolutionize TDF design and reposition the messy middle as a Goldilocks zone-neither too volatile for prudence nor too stagnant for real growth.

***Disclaimer: The contents of this article should NOT be interpreted as financial or investing advice. Rather, to be viewed as an exploratory educational piece***

Accelerating Institutional Cryptocurrency Adoption

Institutional investors are increasingly recognizing the value of alternative asset exposures, with Bitcoin ETFs like BlackRock’s IBIT reaching $70 billion in assets within 341 days - five times faster than the previous record held by SPDR Gold Shares. However, institutional Bitcoin ETF holdings declined 23% in Q1 2025 amid price volatility, highlighting the need for more stable cryptocurrency exposure mechanisms. The institutional cryptocurrency landscape has experienced explosive growth overall, with spot Bitcoin ETF assets reaching $104.1 billion by Q4 2024, marking a 77% quarterly increase. Yet this adoption trajectory reveals critical volatility constraints that limit broader institutional participation, as exemplified by Millennium Management’s 41% reduction in Bitcoin ETF holdings during Q1 2025 - illustrating the volatility tolerance challenges facing sophisticated institutional investors.

Professional investors now hold $27.4 billion in Bitcoin ETFs, representing 26.3% of total assets under management and marking a 114% quarterly increase. Despite this surge, institutional allocations declined for the first time in Q1 2025, underscoring the urgent need for volatility-managed cryptocurrency exposure. Hedge funds have emerged as the largest institutional holders, accounting for 41% of all holdings, with Millennium Management leading at $2.6 billion across six products. This concentration among volatility-tolerant investors underscores the market opportunity for stability-enhanced alternatives.

Further compounding the challenge, the collapse of the futures basis trade - from 15% annualized premiums to near zero by Q1 2025 - has eliminated a key institutional entry mechanism, further emphasizing the need for alternative approaches to cryptocurrency exposure. Nevertheless, sovereign entities like Abu Dhabi’s Mubadala, with a $409 million IBIT stake, demonstrate that institutional interest grows when appropriate risk management tools become available.

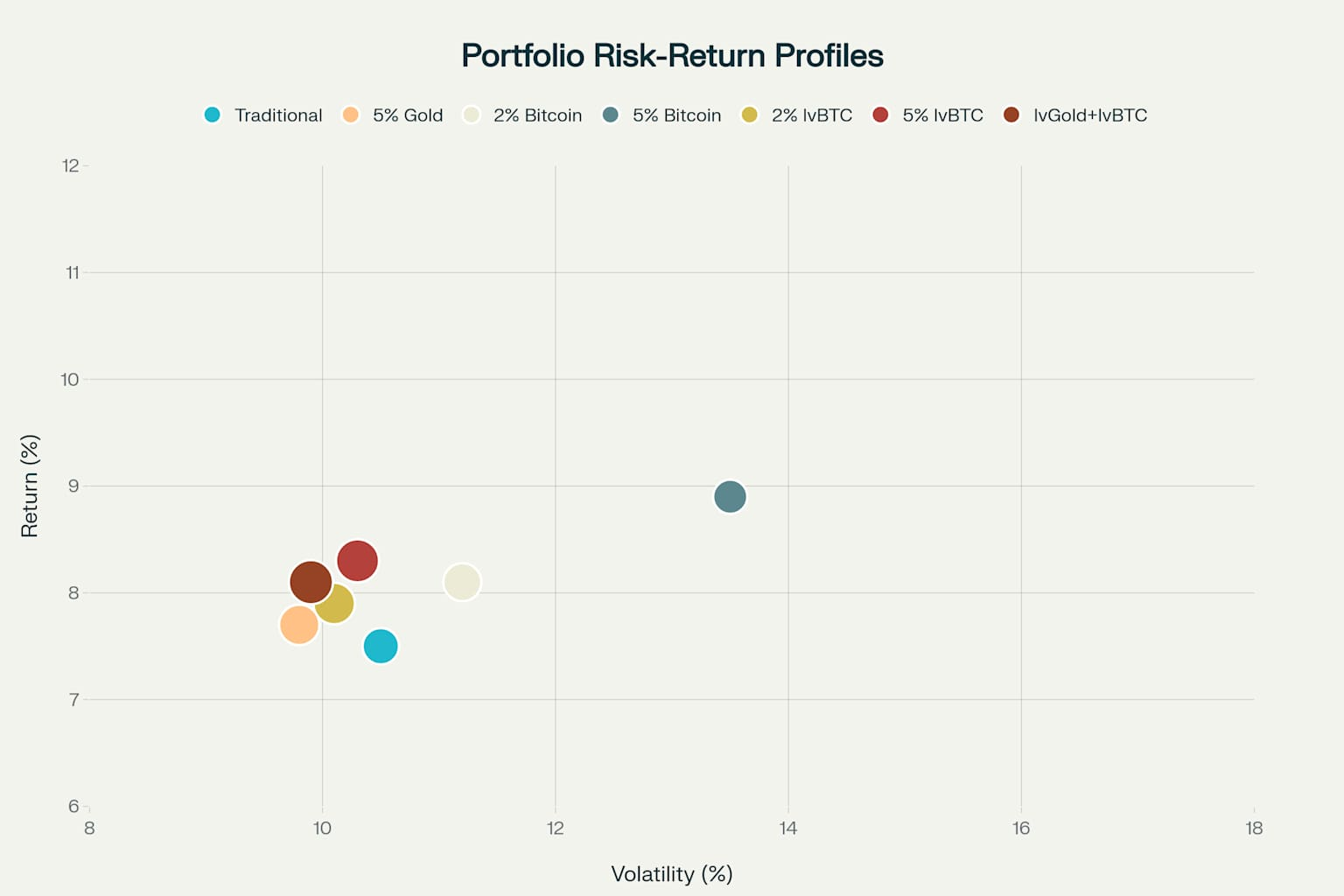

The risk-return analysis demonstrates that portfolios incorporating low-volatility derivatives can achieve superior Sharpe ratios compared to traditional allocations. LVAs offer the potential for enhanced returns with reduced volatility, addressing institutional requirements for both performance and risk management.

The Missing Asset Problem

Traditional portfolio construction relies on a limited set of ingredients, constraining potential outcomes for retirement savers. Fiat currencies provide near-term stability but suffer from inflation erosion and censorship risks, while commodity-monies like Bitcoin and Gold offer inflation protection but exhibit excessive volatility for commercial use. Ampleforth's LVAs solve this dilemma by creating synthetic commodity-monies with significantly reduced volatility characteristics.

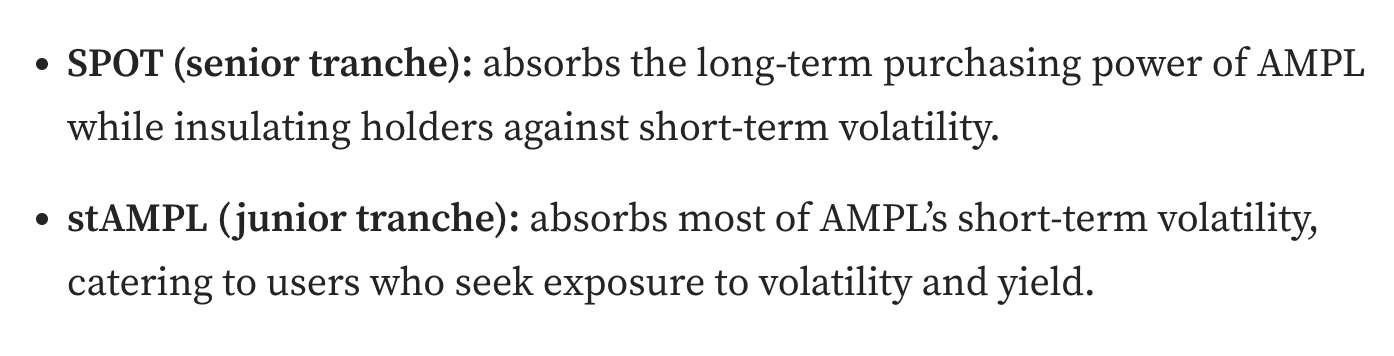

The SPOT protocol achieves this through perpetual derivative contracts that continuously recycle fixed-term tranches. Senior tranches (SPOT tokens) absorb minimal volatility while junior tranches (stAMPL) act as volatility sponges, creating a sustainable system where stability is achieved through market-supported mechanisms rather than centralized control.

The Art of Strategic Asset Allocation

Core Principles of Strategic Asset Allocation

Strategic Asset Allocation (SAA) represents the systematic determination of target allocations across asset classes based on risk tolerance, time horizon, and investment objectives. Unlike tactical approaches focused on short-term market timing, SAA establishes long-term portfolio foundations designed to optimize risk-adjusted returns over complete market cycles. The framework requires periodic rebalancing to maintain target allocations as market movements cause portfolio drift.

Modern SAA frameworks increasingly incorporate alternative assets to enhance diversification and improve return profiles. Institutional investors have historically maintained 25% alternative allocations compared to 5% for advisors, driven by superior access and operational capabilities. However, traditional alternatives often introduce liquidity constraints and complexity that limit their applicability in dynamic portfolio construction.

LVAs represent a revolutionary improvement - or rather, enhancement - to SAA frameworks by providing commodity-money exposure without traditional volatility constraints. This innovation enables institutions to achieve strategic commodity allocations while maintaining operational flexibility and risk management capabilities without the manual overhead. The perpetual nature of LVA derivatives eliminates rollover costs and timing risks associated with traditional commodity strategies.

In terms of implementation, from an SAA standpoint, a plausible approach would be for institutions to consider replacing portions of existing alternative allocations rather than expanding total portfolio risk. For example, implementing 5-10% total LVA allocations divided between 2-5% lvBTC for growth exposure and 3-7% lvGold for stability enhancement.

Core-Satellite Approach

The core-satellite approach represents a sophisticated portfolio construction methodology that combines passive, diversified "core" holdings with active, targeted "satellite" positions designed to enhance returns or manage specific risks. This framework enables institutions to maintain broad market exposure through low-cost index strategies while capturing alpha opportunities through specialized allocations.

Core allocations typically comprise 60-80% of institutional portfolios, consisting of diversified equity and fixed income exposures that provide market-level returns with minimal tracking error. These positions emphasize cost efficiency, tax optimization, and consistent performance across market cycles. Satellite allocations, representing 20-40% of portfolios, target specific opportunities including alternative assets, sector concentrations, or geographic tilts.

LVAs function optimally as satellite allocations due to their unique risk-return characteristics and diversification benefits. Unlike traditional satellites that often increase portfolio volatility, LVAs provide growth exposure while potentially reducing overall portfolio risk through superior risk-adjusted returns. This combination enables institutions to enhance expected returns without proportionally increasing portfolio volatility

Sophisticated institutions implement LVAs as diversification-enhancing satellites that complement rather than compete with core allocations. The optimal structure allocates 5-8% to lvGold as an inflation protection satellite and 2-5% to lvBTC as a growth enhancement satellite. This allocation provides meaningful exposure to commodity-money benefits while maintaining portfolio stability through volatility reduction mechanisms.

The satellite positioning enables institutions to benefit from LVA innovations while limiting concentration risks. Portfolio rebalancing protocols maintain target allocations while capturing the volatility reduction benefits of LVA derivatives. Dynamic satellite management allows institutions to adjust LVA exposures based on market conditions and portfolio requirements.

Implementation benefits from LVA compatibility with existing satellite strategies, including real estate, infrastructure, and private equity allocations. The digital asset structure enables rapid rebalancing and tactical adjustments that enhance portfolio agility compared to traditional illiquid alternatives. This operational flexibility supports sophisticated satellite management strategies while maintaining institutional governance standards.

Enhancing Target Date Funds (TDFs)

Target Date Funds managing $4.3 trillion in assets face fundamental structural limitations that constrain portfolio optimization. Traditional glide paths rely primarily on equity-bond allocations with minimal alternative asset exposure, creating binary risk-return trade-offs as participants approach retirement. This conventional framework generates a sequence of returns risk, inflation exposure, and limited diversification benefits that potentially compromise retirement security

The traditional approach implements linear equity reduction from 90% at career inception to 20% post-retirement, with corresponding bond increases. This binary framework fails to address inflation protection requirements, duration risk management, and optimal risk-adjusted return generation. Academic research demonstrates that alternative glide path designs incorporating real assets and alternative investments can significantly improve retirement outcomes.

Current TDF design faces particular challenges from low bond yields that inadequately compensate for inflation risk and duration exposure. The conventional framework forces participants into suboptimal choices between accepting inadequate returns through bond-heavy allocations or embracing excessive volatility through equity concentration. LVAs provide a revolutionary solution by enabling TDFs to access commodity-money benefits without traditional volatility constraints.

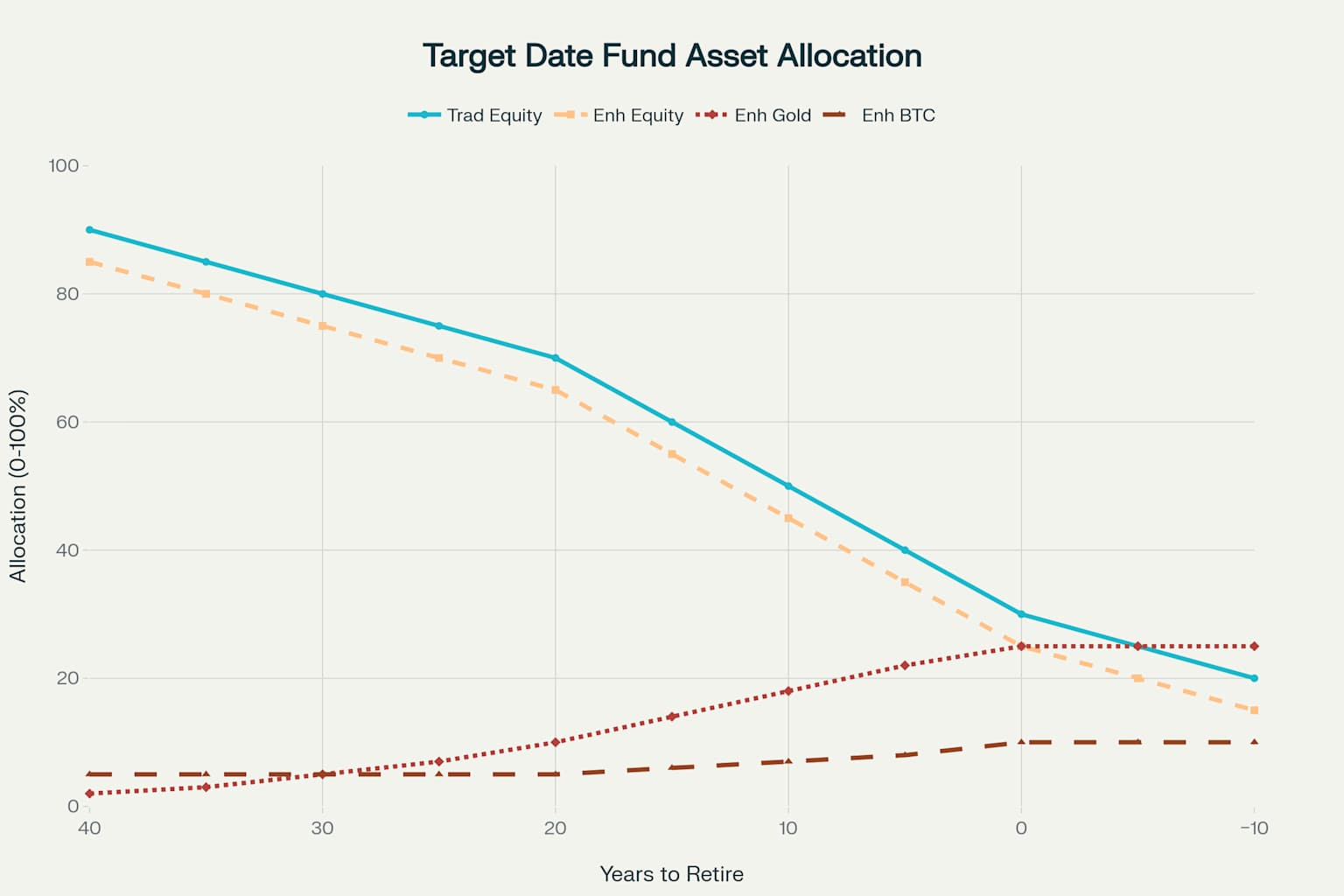

The enhanced TDF framework implements sophisticated LVA integration that evolves strategically throughout the participant lifecycle. Unlike traditional binary equity-bond transitions, the enhanced approach incorporates increasing LVA allocations as retirement approaches, maximizing inflation protection when participants most require stability. This design recognizes that retirement security depends on purchasing power preservation rather than nominal value maintenance.

The enhanced glide path initiates with 5% lvBTC and 2% lvGold allocations during early accumulation phases, providing growth exposure with reduced volatility. Mid-career transitions gradually increase lvGold allocations to 10% while maintaining lvBTC exposure for continued growth potential. Pre-retirement phases accelerate lvGold increases to 18% while reducing equity concentrations, creating inflation-protected stability during a critical sequence of returns periods.

Post-retirement implementation maintains substantial 25% lvGold allocations combined with 10% lvBTC exposure, ensuring continued purchasing power protection during distribution phases. This allocation provides superior inflation protection compared to traditional bond-heavy post-retirement portfolios while maintaining reasonable volatility characteristics. The enhanced framework enables TDF participants to achieve retirement security through commodity-money stability rather than nominal value preservation.

The $2.1 Trillion Opportunity

The LVA addressable market represents one of the most significant investment innovation opportunities in modern financial history, with conservative projections indicating $2.1 trillion in potential allocations by 2030. This opportunity stems from convergent trends, including expanding alternative asset adoption, growing cryptocurrency institutional acceptance, and increasing demand for inflation-protected investment solutions

The Target Date Fund segment alone represents $4.3 trillion in current assets, with continued growth projected to reach $6.8 trillion by 2030. Conservative LVA penetration estimates of 5-10% within TDF portfolios generate $340-680 billion in potential allocations from this single segment. The institutional alternatives market, currently managing $8.5 trillion and projected to reach $15.2 trillion by 2030, provides additional adoption opportunities as institutions seek enhanced diversification solutions

Alternative Investment Funds managing $12.8 trillion globally and projected to reach $25.8 trillion by 2032 represent a particularly compelling adoption pathway. These sophisticated investors actively seek innovative strategies that enhance risk-adjusted returns while providing uncorrelated exposure to traditional asset classes. LVAs align perfectly with AIF objectives by providing commodity-money exposure through volatility-managed derivatives that enable optimal portfolio integration.

Conclusion

Low-Volatility Assets are a fascinating lesson in how progress often comes from rethinking what’s always been there. For decades, the idea that you had to choose between volatility and stability was a given - as if you could either have excitement or security, but never both. LVAs flip that idea on its head by showing that stability isn’t about avoiding change; it’s about managing it with discipline (and most importantly, risk preference). They’re a reminder that in finance, and in life, the best solutions are usually about harnessing the inevitable forces around us - like volatility and inflation - rather than pretending they don’t exist. By creating assets that are durable, inflation-resistant, and predictable, LVAs offer a glimpse at what happens when you stop fighting the tide and start surfing it. Offering a re-imagination of what money and portfolio management can be. In the end, that’s what makes them so powerful: they meet the basic human need for safety and growth at the same time - something that’s rare in any economy, and almost unheard of in DeFi, and especially in TradFi, until now.